The Term Structure of Interest Rates

April 2, 2026

Interest rates change over time. Central banks use them as a tool to drive the economy in the direction they intend. Market perception of risk shifts the spreads between risk-free and risky bonds.

Bond prices and values are sensitive to changes in interest rates, therefore we need to have a good understanding of the impact of and sensitivity to changes in interest rates to make better investment decisions.

Pricing and valuation models in Finance are based on the principles of time value of money and no-arbitrage pricing. Let me define common terms before we get started.

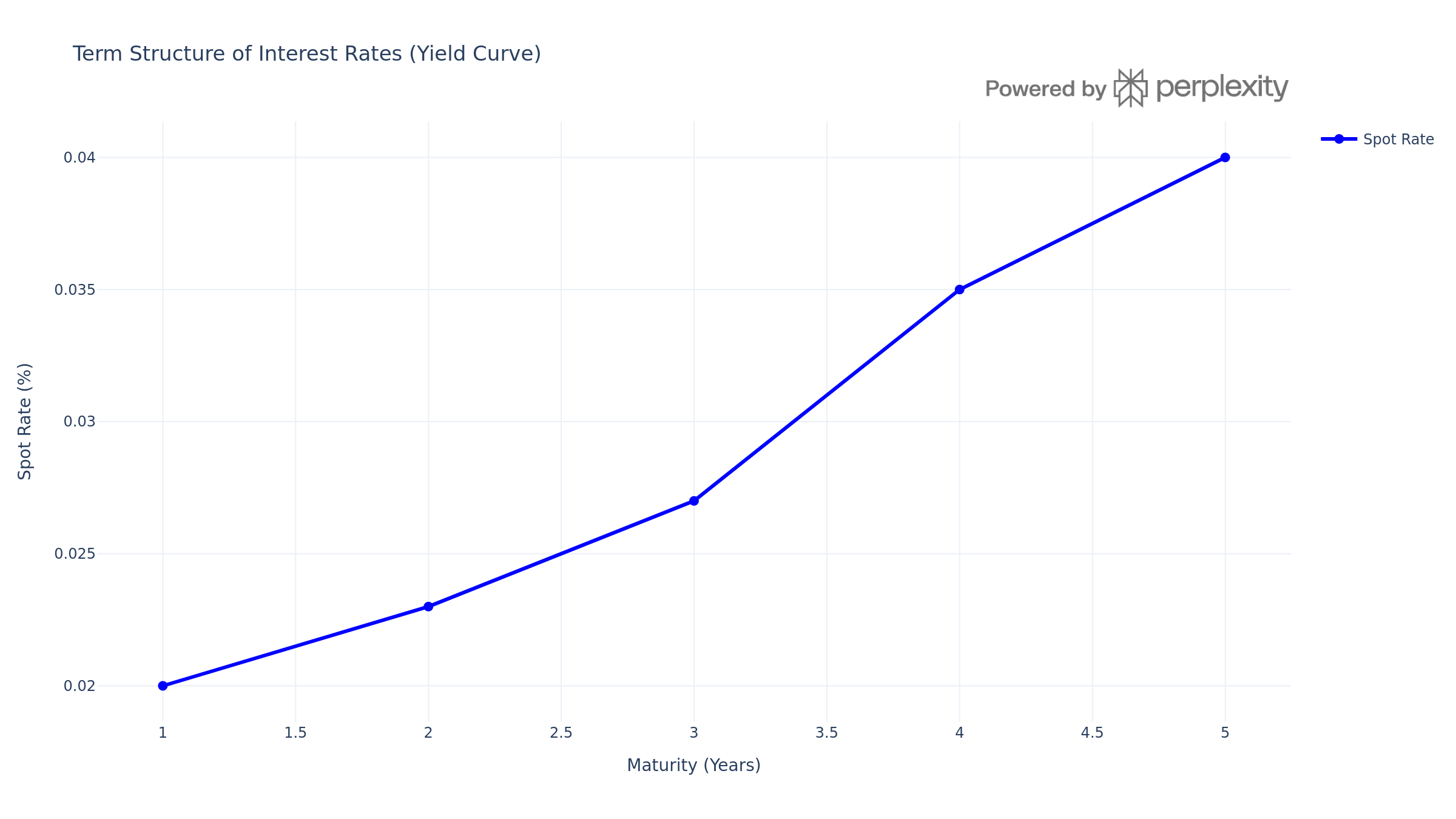

Spot Rates: These are the interest rates for periods. For example, a 2-year spot rate, is used to discount cash flows occuring 2 years from now.

Par Rates: [TODO]

Forward Rates: [TODO]

Zero Rates: [TODO]

Term structure of the interest rates refers to the evolution of interest rates over time. The concept of term structure is explained visually in all texts I have seen and for a good reason. The following table and chart illustrate the concept.

The graph above is called a spot yield curve. Have a good look at it—memorize it—because we are going to have a painstakingly long discussion on this.